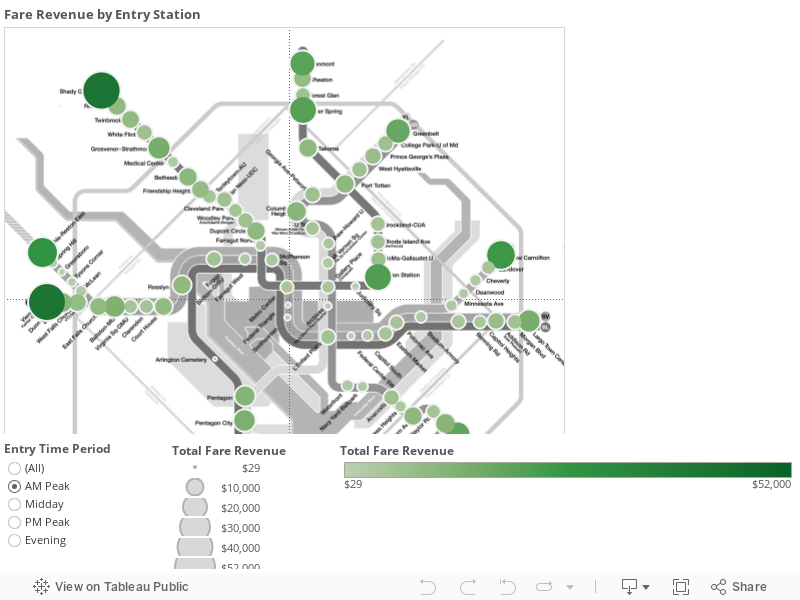

Metrorail Revenue by Station – Visualized!

Where and when does Metrorail generate the most farebox revenue? So far the data reinforces the notion that ours is a truly regional system with strong revenue contributions from all jurisdictions – but of course, the story is far more complicated than that…

What kind of rail system is Metrorail? Urban subway? Commuter rail? Hybrid? The answer of course is all of the above. And if that is the case, what kind of ridership and revenue patterns should its stations and system exhibit? High levels of peak revenues with heavy commuter lot usage but relative inactivity during the day? Lower levels of peak period activity but a steady stream of usage throughout the day? Depending on your perspective (and travel patterns) one might argue for either, and it might seem easy to apply a blanket classification to Metrorail and declare that “only urban stations cover their cost” or “commuter stations contribute largely to Metrorail’s revenue picture.”

Well, when you throw the data up on a map, it becomes clear that there are no easy answers, and no one right way to view the revenue picture of our tri-jurisdictional hybrid rail network. Some conclusions from the data are intuitive, some less so. Among them:

- Differences in ridership across stations are bigger than differences in revenue, so ridership is a stronger explanation of differences in revenue than fares. For example, Shady Grove’s average fare in the AM Peak is $5, which is twice as much as the smallest average fare. On the other hand, ridership at Shady Grove is ten times higher than other stations, so the ridership better explains the station’s revenue.

- In the AM Peak, the terminal stations dominate in terms of revenue contribution. Union Station functions as an internal “terminal station,” meaning that the commuter rail and Amtrak connections to Metro are extremely important to the overall ridership and revenue picture.

- Other stations with strong bus or commuter park-and-ride infrastructures also pop in the AM Peak, such as Silver Spring and Grosvenor.

- Note how well the non-Silver line stations in Virginia perform in the AM Peak, as well as the somewhat expected better performance of the Shady Grove branch of the Red Line in the AM Peak.

- In the PM Peak, the core is king. Stations like Farragut West and North, Metro Center, L’Enfant Plaza are producing $50,000 apiece every evening thanks to their job densities, reinforcing the importance of improving their capacity for the future in Metro 2025, as well as their huge importance to revenue today. By comparison, in the AM Peak, only Shady Grove and Vienna approach these levels of revenue at roughly $40,000 per station.

- The New Carrollton and Largo Town Center branches of the Blue/Orange/Silver Lines contribute significantly less revenue than other branches, and this directly relates to the relative lack of transit-oriented development along these spines. The station areas on these lines enjoy a superb level of rail connectivity to the region’s primary job cores, but without sound transit-oriented investments to-date, they have not yielded the type of ridership and revenue commensurate with the capital investment. Imagine what Metro’s revenues (and farebox recovery) could look like if these segments were properly developed!

We’ve been examining the data ourselves as we continue forward with Momentum’s call for us to ensure financial stability for the Authority and have created the visualization for you to play with. We’d love to know what you see!

The conclusions you’re drawing in this article are made without looking at all of the data. When you select “all” on your map, it becomes clear that very few suburban stations come close to producing the revenue of stations in D.C. In fact, only two stations outside of D.C. yield more than $55k in revenue compared with seven in the District. Six of those seven yield over $60k in revenue – no suburban or exurban station can claim that. The difference is probably that District residents are more likely to use Metro outside of their work commute.

Putting stations in Georgetown, Logan Circle, Adams Morgan, and on H Street would yield a LOT more revenue than extending Metro further into the suburbs. They’d also be more expensive to build, sure, but the costs would be recouped rather quickly and since the stations are closer together it’s less track to maintain.

As an illustration – compare revenues at the stations near Georgetown (ranging from $54k-71k), which should be somewhat predictive of what we’d see with a Georgetown Metro station (Georgetown would probably be higher, actually, since it’s such a big tourist and shopping destination), to the average revenue for the new silver line stations (about $13k or less than 1/4 of what the stations closest to Georgetown yield). Once you spread these differences over a decade, the difference is positively staggering. Supposing that a Georgetown or H Street station was on the low end of the averages for busy D.C. stations, we’re talking about $47M in revenue for the typical Silver Line station over a decade, versus $197M for a D.C. station.

Given the costs of the Silver Line thus far, it will take each station an average of 120 years to pay for itself. Compare this, too, with the cost of the NY Ave Metro, which cost about $130M in today’s dollars but brings in $8.7M in revenue per year – at that rate it pays for itself in about 14 years.

Exurban Metro rail, with few exceptions, is a TERRIBLE investment.

I think there’s still more to the story. The stations with the highest revenue must be, generally, one end of round trips. So the revenue generated at DC stations isn’t just a matter of people boarding Metro; they’re almost all going someplace or returning to someplace.

@Anonypants

You need to remember the core stations get 2-3 times more service than the suburban stations. Example: Vienna – 5.5 minute peak headway, Farragut West 2 minute peak headway.

Silver Line is doing pretty well for only being open 9 months compared to 30+ years for most core stations.

Hi there –

The discussion here and @GGW is fabulous and highlights the challenges that we face in over-simplifying the structure of our rail network. I believe that GGW did a nice piece a year and a half back articulating the unique nature of Metrorail – which is part commuter rail, part urban subway. The revenue patterns that we see in the maps simply reflect that nature.

@ Anonypants and @mcs (and @SteveDunham) –

The thing to remember here is the importance of work-based destinations for many of the trips on Metorail, and the fact that the bulk of workplace destinations are in the downtown cores of the region. Meanwhile, the spokes tend to feed riders into the system headed for the core. So the system picks up passengers from its spokes (much like a collector road) and deposits them in the core in the AM, with the reverse pattern taking place in the PM. AM peak entries, then, will show lower per-station revenue volumes because each one is picking up a portion of the overall passenger volume on the system. In the PM peak, when all of those passengers are getting back on the system, they use a fewer number of stations to board, and concentrate their station-based revenue at these stations.

This just goes to show us that regardless of where we live, we all contribute to core capacity usage and all need to contribute to alleviating crowding in the core!

@Anonypants

No offense, but exurban MetroRail looks to be a fantastic investment when one actually looks at the ridership patterns. With the exception of the Red Line up Conn ave, most of the DC system beyond the core is middle of the road with Virginia being the cream of the crop and PG county bringing up the rear. Metro’s split is East-West, not Urban-Suburban. VA should take a more leading role in expanding the both the Metro’s Core Capacity and outer reaches. If they could partner with DC, I bet funding for splitting the Blue, Orange and Silver lines off onto their own corridors in Central DC could be found.

@Anon

Citation needed. I’ve at least provided real numbers to back up my assertions.

Don’t get me wrong – rail is a GREAT investment for suburban/exurban areas around D.C. But trying to make Metro do double duty as a city subway and commuter rail causes a lot of problems, from maintenance to coordinating with an increasing number of jurisdictions for things like funding.